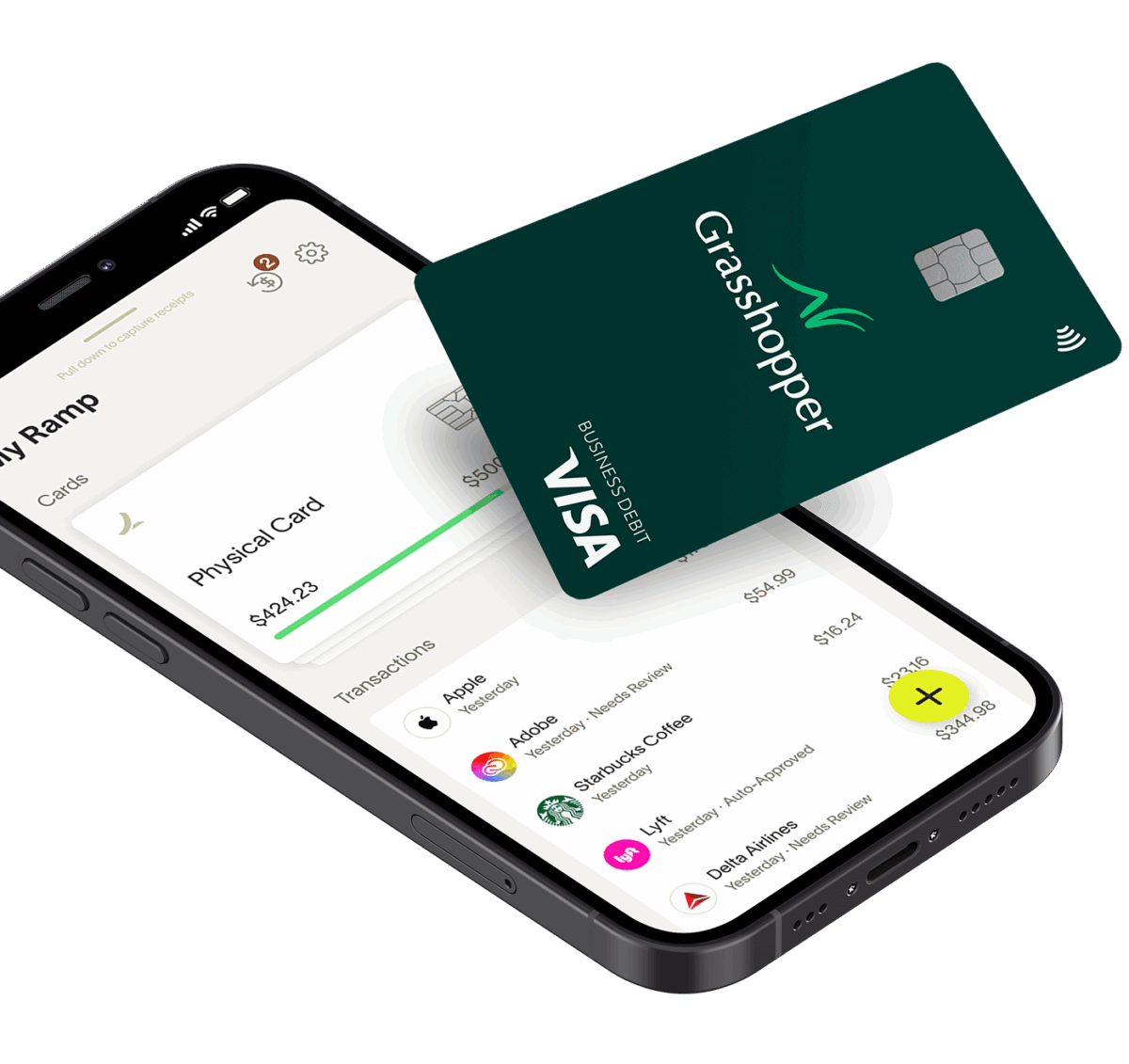

Ramp Corporate Card Review

Earn 1.5% cashback with an annual fee of $0.00.

Advertisements

Benefits and Features

Unlimited 1.5% flat cashback

No personal guarantee required

Automated expense management tools

Zero foreign transaction fees

The Ramp Corporate Card is a premier financial solution for modern enterprises seeking to optimize treasury management and business finance.

Unlike traditional credit products, it integrates a high-performance payment tool with an elite expense management platform. This ecosystem is specifically engineered for registered US entities that prioritize accounting automation and financial discipline.

Key benefits for scaling companies:

- Liability Shield: No personal guarantee required, protecting your personal assets.

- Smart Software: Automated expense tracking and real-time receipt matching.

- Total Control: Instant issuance of virtual cards with customizable spending limits.

- Global Acceptance: Seamless operations on the worldwide Visa network.

By eliminating month-end friction and providing deep insights into corporate spending, this platform serves as a comprehensive command center for your organization’s growth. It is the definitive choice for founders who value efficiency and scalable financial infrastructure.

Love what this card offers? Just click the button below to get started.

About the Issuer: Ramp

Ramp Business Corporation emerged in 2019 as a powerful disruptor in the corporate finance space. Founded by Eric Glyman, Karim Atiyeh, and Gene Lee, the New York City-based company operates as a modern financial technology firm rather than a traditional legacy bank.

To provide its core corporate card products, the company utilizes a hybrid approach, partnering with established financial institutions like Celtic Bank and Sutton Bank to issue its Visa network cards.

Unlike traditional issuers that often generate revenue through interest charges and obscure fees, this fintech firm positions itself as an automated finance platform designed to actively help businesses identify savings and streamline month-end accounting. Its trust signals are deeply rooted in its impressive scale and comprehensive product suite.

Today, the platform serves tens of thousands of businesses across the United States, backed by a robust infrastructure that includes continuous 24/7 customer support, accounts payable automation, and advanced procurement tools.

Who This Card Is For (And Who Should Avoid It)

The ideal customer profile for this corporate charge card centers entirely on well-funded, registered US entities such as corporations, LLCs, and LPs. Fast-growing tech startups, digital marketing agencies, and scaling mid-market enterprises that process high transaction volumes are the perfect fit.

For instance, a venture-backed software company needing to issue secure, unlimited virtual cards to different departments for server costs, advertising budgets, or employee travel will find immense utility in the platform's automated spend management features.

Conversely, several business types must explicitly avoid this card due to fundamental data fit issues and strict underwriting protocols. If you operate as a sole proprietor or an unincorporated partnership, you are strictly ineligible and should bypass the application completely.

Crucially, companies maintaining less than $75,000 in liquid cash within a linked US business bank account will be automatically rejected.

Furthermore, companies that need the flexibility to finance large purchases over several months must look elsewhere; as a strict charge card, balances must be paid in full at the close of every billing period.

Finally, businesses actively trying to build their commercial credit history should avoid this option, as payment activity is not reported to major commercial credit bureaus like Dun & Bradstreet, Experian Business, or Equifax Business.

Decision Guidance: Weighing the Trade-Offs

Making a final decision regarding this corporate platform comes down to weighing your company's cash flow stability against the need for sophisticated, automated spend controls.

If you have evaluated these constraints and your organization comfortably meets the financial thresholds, this ecosystem represents one of the most efficient ways to modernize your corporate treasury. Continue to the next section for comprehensive application guidance, where we will outline the specific business documentation and steps required to finalize your onboarding.

My Best Buy Visa Card Review

A retail rewards card for frequent Best Buy shoppers who want to compare store rewards, everyday earning categories, and financing trade-offs before applying.

Read the review